Date

Feb 28, 2026

Category

Uncategory

I had a conversation this week that keeps replaying in my head.

It was with someone who works closely with people facing cancer, dementia, and serious illness. The kind of person who is deeply compassionate. Thoughtful. Grounded. The type you’d trust in a crisis.

But then the topic shifted to money.

And something changed.

The language became sharper. Less gentle.

It turned into:

People getting “used to” benefits

People not thinking ahead

People being irresponsible

People spending without control

I didn’t challenge it in the moment. I just noticed it.

How fast empathy disappears when money enters the room.

We don’t blame people for getting sick.

We don’t shame people for needing care.

But when someone struggles financially, we often assume it’s their fault.

Why?

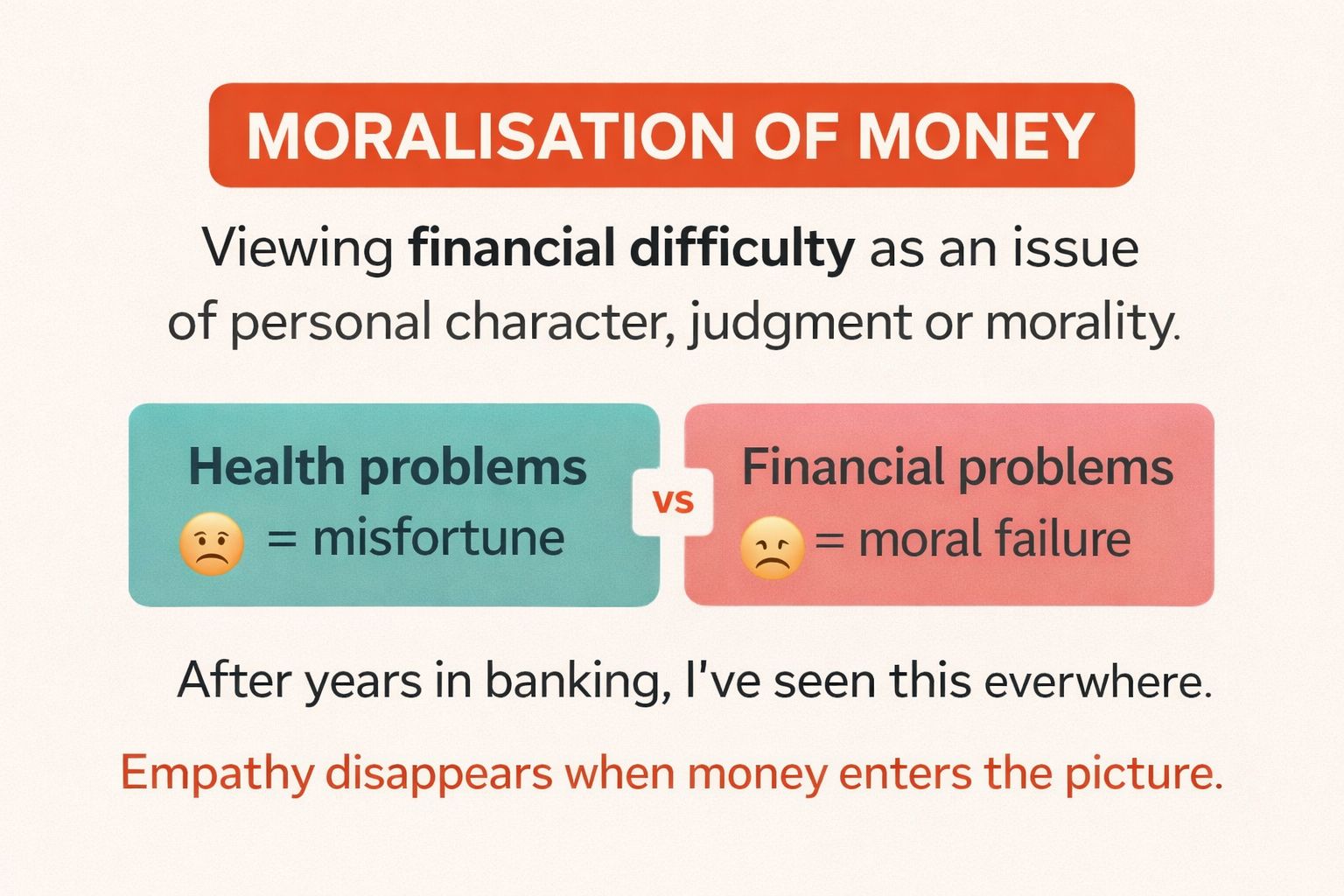

After years of working in banking, I’ve seen this mindset everywhere. Systems built on the belief that people just need more discipline. More education. More self-control.

Underlying it all is an assumption: people are rational. If they’re not succeeding financially, they must be doing something wrong.

But that’s not how humans work.

When someone feels overwhelmed:

Their cognitive bandwidth shrinks.

Long-term thinking becomes harder.

Avoidance increases.

Shame blocks action.

This isn’t irresponsibility. It’s what happens under pressure.

There’s a phrase for what we do culturally: the moralisation of money.

Health problems are seen as misfortune.

Financial problems are treated as moral failure.

And that framing shapes how we design financial systems.

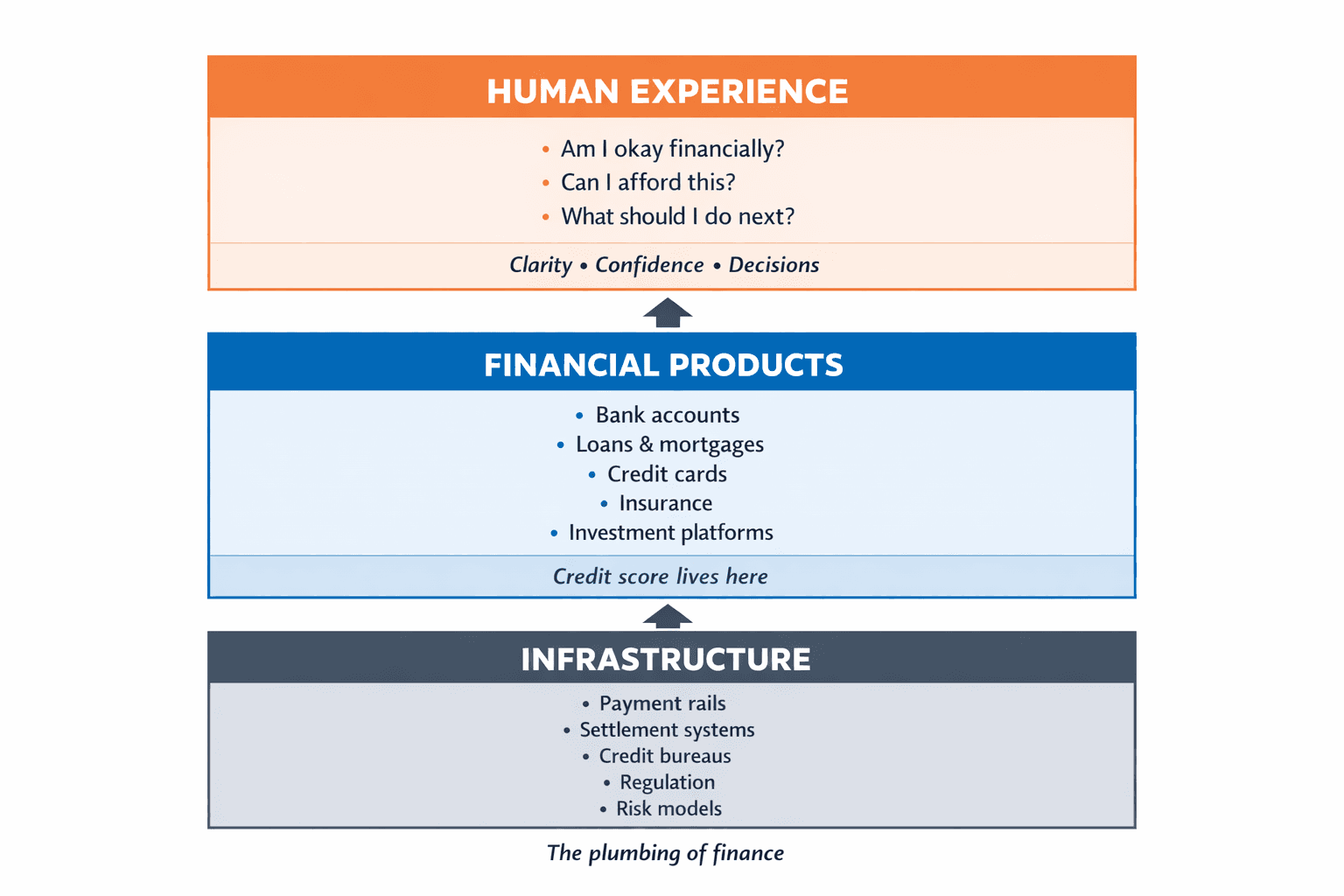

Most financial products are built for calm, analytical, spreadsheet-thinking people. Not for someone who is scared. Or exhausted. Or juggling too much. Or trying not to look at their balance because it makes their chest tighten.

This is the core question driving my current research:

What would financial products look like if they were designed for humans under pressure?

Not idealised consumers.

Not perfectly rational decision-makers.

Actual people.

I don’t think helping someone feel in control of their money is about pushing discipline harder. I think it’s about reducing fear. Increasing clarity. Restoring dignity.

And I’m increasingly convinced this is one of the biggest missed opportunities in finance.

The organisation that genuinely helps people:

feel safe with money

understand where they stand

take one clear next step

move forward without shame

won’t just improve customer outcomes.

It will earn something far more valuable than interest or fees.

Trust.

And trust compounds.

Go Back