Healthy Borrowing (Debt Clarity & Early Intervention)

Helping customers understand and act on their debt earlier, before reaching crisis points

Company

UK regulated lender

Date

2024–2025

Project Overview

Context

In the UK, millions of people are slowly falling into debt without really realising it. It rarely happens because of one big mistake. It happens through everyday decisions, life events, unclear signals, and products that are hard to understand. By the time customers reach collections, many feel overwhelmed, ashamed, or stuck.

When I started this work, the organisation was doing what most lenders do: stepping in late, focusing on risk and arrears rather than on how people actually experience borrowing in their day-to-day lives.

This project was about shifting that mindset. Instead of asking “how do we manage risk?”, we asked “how do we help people understand their debt earlier and feel more in control of it?”

It sits at the heart of the bank’s Caring Banking strategy and connects directly to my wider work on how people relate to money, which also forms the basis of my dissertation.

Key Highlights

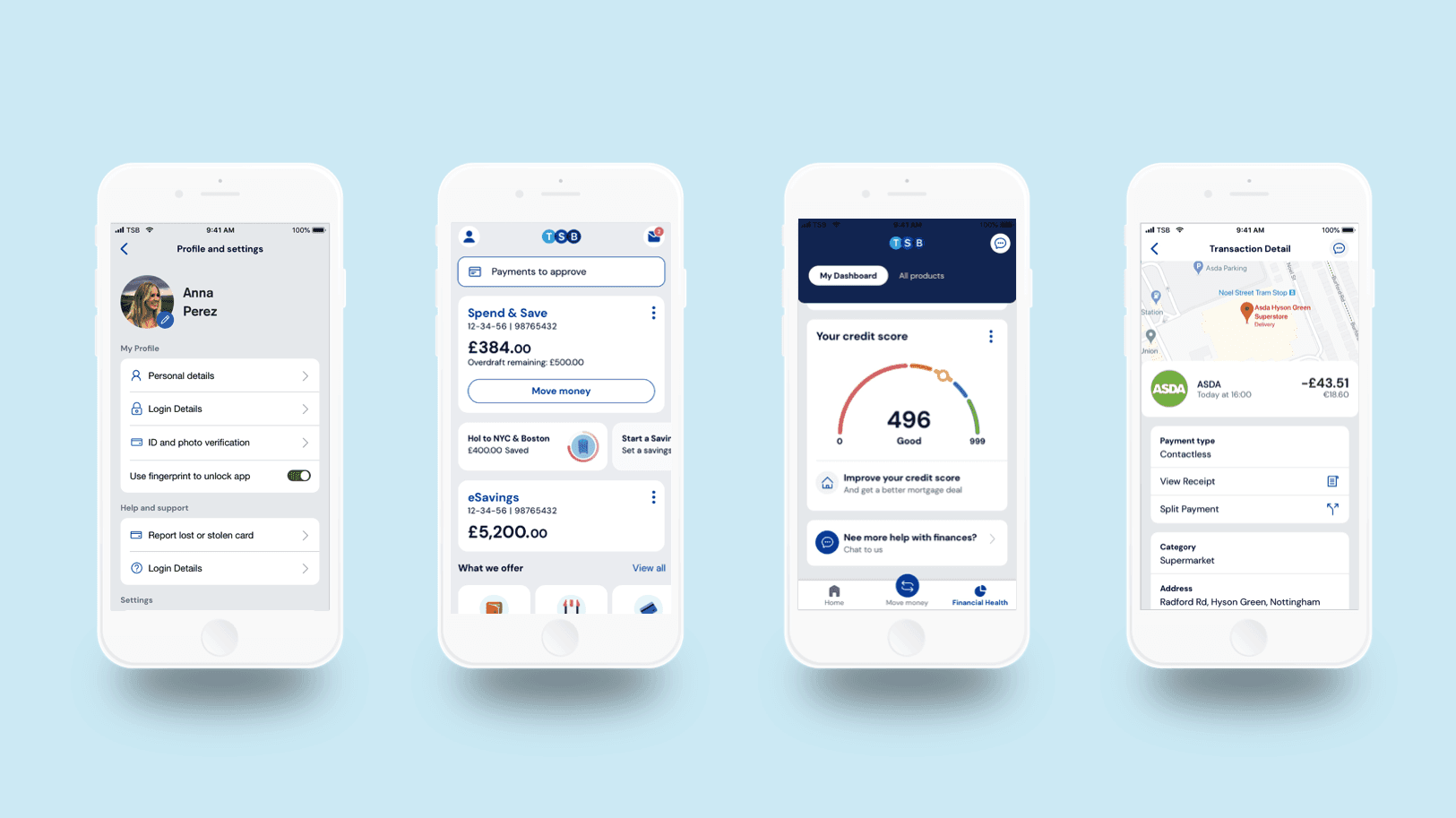

I worked closely with product, risk, collections, data, and operational teams to bring a shared view of borrowing health into everyday decision-making.

Together, we:

Mapped how customers gradually move from manageable borrowing into stress and loss of control, often without clear moments of awareness

Identified early signals where small, supportive interventions could make a real difference

Brought customer stories to life to help teams understand what debt actually feels like for people, not just what it looks like in numbers

Shifted conversations away from “fixing problems late” towards designing for understanding, clarity, and prevention

Applied this thinking across multiple areas, including credit cards and vehicle finance, where long-term debt can quietly build over time

Rather than designing a single product or journey, this work focused on shaping how the organisation thinks about borrowing, vulnerability, and responsibility.

Service Design · Customer Experience Strategy · Behavioural Design · Design Leadership

Key Highlights

Outcomes

Introduced a shared framework for “borrowing health” used across product and risk teams

Drove changes in app journeys and communications to support earlier customer action

Embedded customer insight into decision-making, especially in vehicle finance and in-life servicing

Improved alignment between product, risk, and collections around customer outcomes

Increased focus on early intervention over reactive collections

Contributed to clearer, more supportive in-app experiences for customers managing debt

Why this matters

Debt isn’t a failure of discipline. It’s often a failure of understanding.

When people feel more in control of their money, they make better decisions, and organisations build more sustainable relationships in return.

Go Back